.png)

Nothing is certain except for taxes and annual inflation adjustments by the Internal Revenue Service (IRS) for health savings accounts (HSAs). Ok, that's not how the quote goes, but the IRS did release its annual updates for HSAs in 2026 with the publication of Rev. Proc. 2025-19. In this article, we'll review the updated contribution limits and high-deductible health plan (HDHP) requirements, and compare 2026 adjustments with past adjustments. Let's dive in!

2026 HSA contribution limits

Account holders can deposit pre-tax funds into their HSA up to their respective contribution limits. In 2026, the individual and family contribution limits will both increase.

.png)

Contribution limits for self-only coverage will increase by $100 to $4,400, a 2.33% increase from last year. Contribution limits for family coverage will increase by $200 to $8,750, a 2.34% increase from last year. With higher limits, account holders can protect more of their annual income from payroll taxes and use those savings for healthcare expenses.

2026 Minimum deductible and out-of-pocket maximum amounts

To contribute to an HSA, the IRS requires account holders to:

- Not be enrolled in Medicare

- Not be claimed as a dependent on someone else's tax return, and

- Be covered by a federally defined high-deductible health insurance plan on the first day of the month

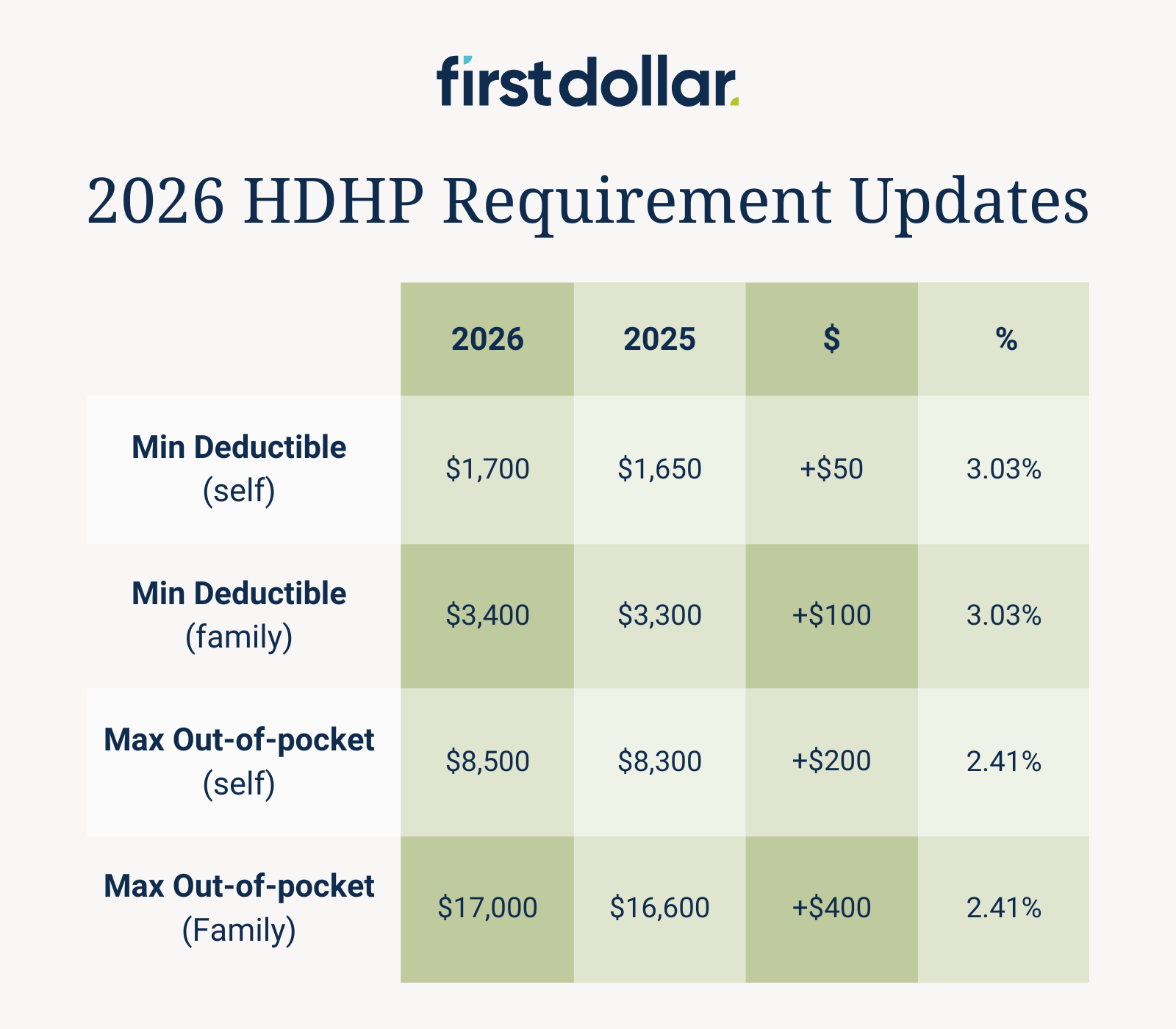

Last week, the IRS updated its requirements for high-deductible health plans (minimum deductibles and maximum out-of-pocket expenses) for account holders in 2026.

For individuals with high-deductible health plans in 2026, the minimum deductible will increase by $50 to $1,700 for a year-over-year increase of 3.03%, while the maximum out-of-pocket expenses will increase by $200 to $8,500 for a year-over-year increase of 2.41%.

For families with high-deductible health plans in 2026, the minimum deductible will increase by $100 to $3,400 for a year-over-year increase of 3.03%, while the maximum out-of-pocket expense will increase by $400 to $17,000 for a year-over-year increase of 2.41%.

What this means

Increases in deductible and out-of-pocket amounts potentially mean more healthcare expenses for account holders in 2026. Account holders can prepare for these potential increases by saving pre-tax funds via contributions to their HSA.

Comparing 2026 contribution limit updates with history

How did the IRS adjustments for 2026 line up with previous years? Let's compare.

IRS economists calculate inflation based on the chained CPI, an index that captures the current cost of goods in the economy. They apply that percentage to HSA amounts (e.g., contribution limits) and round to the nearest $50. If you want to geek out, the 26 U.S. Code § 223 (G) spells out cost-of-living adjustments.

The IRS announces its calculations for the following tax year in May. 2026 adjustments reflect 2025 economic conditions, 2025 adjustments reflect 2024 economic conditions, etc. With that in mind, we can understand why adjustments for 2023 and 2024 jump out on the chart—inflation was historically high in 2022 and 2023.

Conclusion

Next year, amounts for HSA contribution limits, minimum deductibles, and maximum out-of-pocket payments will increase. Contribution limit increases allow account holders to allocate more pre-tax funds for health care costs. In contrast, increases in HDHP requirements will potentially make account holders responsible for additional costs. These annual adjustments are calculated based on inflation conditions.